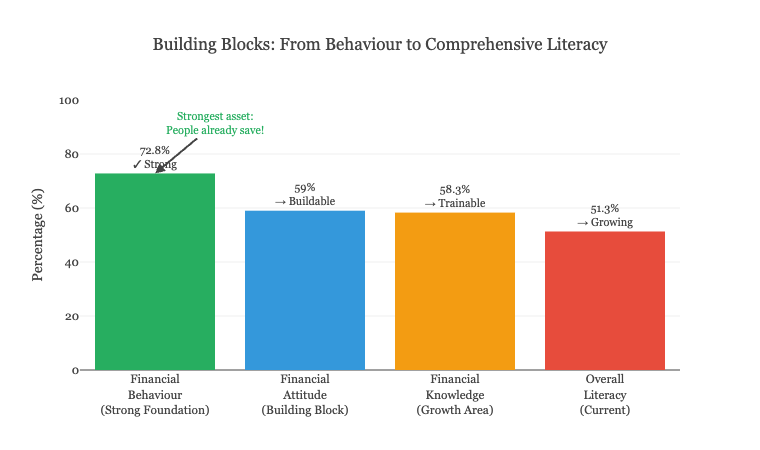

In rural India, where 70% of the nation resides, a remarkable foundation is already in place: 73% of households demonstrate sound financial behaviour, regularly saving and managing their money wisely. This strong foundation presents an unprecedented opportunity to build comprehensive financial literacy across 89.3 million agricultural households.1

Meet Ramesh and Sunita, a farming couple from Madhya Pradesh who represent rural India's evolving financial landscape. Ramesh manages crop loans with confidence (60.6% of rural men have good financial knowledge), while Sunita expertly handles household budgets. Together, they embody the potential: with targeted support, households like theirs can bridge the knowledge-to-behaviour gap and access formal financial services more effectively.1

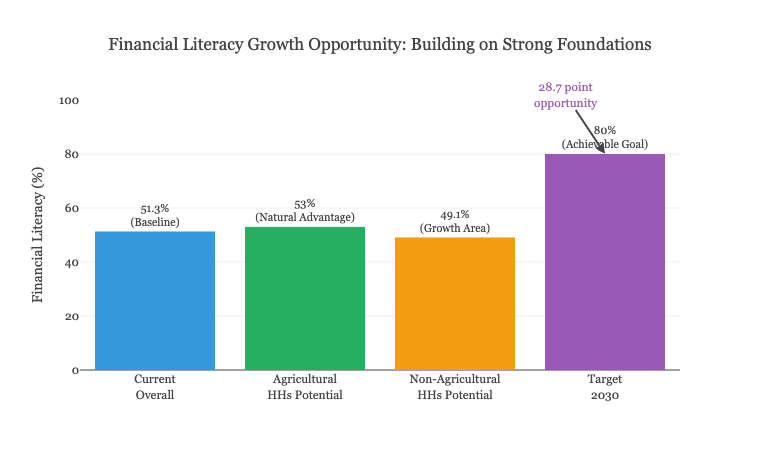

The data reveals an encouraging starting point. Agricultural households already show stronger financial literacy (53%) than non-agricultural ones (49%), thanks to regular banking interactions for credit and insurance.1 This agricultural advantage creates a natural pathway: by strengthening women's financial knowledge in farming households, we can create 47 million financially literate families who manage both farm enterprises and household economies.

The opportunity is particularly promising for women. While 42% of rural women currently possess good financial literacy, the 12 crore women participating in Self-Help Groups represent a ready-made network for rapid scaling.1 Women already demonstrate strong financial behaviour (66% score); with enhanced knowledge and attitude components, they can become powerful financial decision-makers.

The pathway from 51% to 80% financial literacy is achievable within five years. Rural households already save diligently; they need access to the right products and knowledge about their options. Each percentage point improvement represents 890,000 households gaining financial confidence and access to formal services worth approximately ₹50,000 per household annually.

OPPORTUNITY ROADMAP: FROM 51% TO 80% IN 5 YEARS

1. Women's Financial Empowerment Initiative (Target: 5 crore women by 2027): Launch 10,000 financial literacy camps annually, leveraging the existing 12 crore women SHG network. Use successful women entrepreneurs as trainers, creating 50,000 peer educators who earn ₹5,000/month while empowering their communities. Expected outcome: Increase women's financial literacy from 42% to 65%.

2. Digital Financial Inclusion Drive (Target: 10 crore rural users): Deploy vernacular audio-visual content on UPI, digital savings, and micro-insurance via feature phones and community screenings. Partner with 3 lakh gram panchayats to reach the last mile. Expected outcome: 70% digital transaction adoption in rural areas.

3. Agricultural Finance Enhancement Program: Offer interest rate rebates (0.25%) on Kisan Credit Cards when both spouses complete financial literacy certification. This incentivizes 6 crore farming families to pursue joint financial learning. Expected outcome: Agricultural household literacy rises from 53% to 75%.

4. Young Rural Champions Initiative (Target: 1 lakh youth trainers): Recruit educated rural youth (10th-12th pass) as certified financial literacy trainers, paying ₹8,000/month. This creates local employment while building trusted community educators. Expected outcome: 2 crore households trained annually.

5. Gamified Learning Platforms: Develop mobile games and interactive modules in 15 regional languages teaching budgeting, investment basics, and insurance. Partner with telecom operators for zero-rated access. Expected outcome: 3 crore users engaged within 18 months.

6. Success Tracking & Recognition: Create "Financially Literate Village" certification for panchayats achieving 75% household literacy. Provide ₹10 lakh grants for community infrastructure. This creates positive competition and peer learning. Expected outcome: 50,000 certified villages by 2028.

The vision is transformative: by 2030, rural India can become a model of inclusive financial literacy where gender, location, and occupation cease to be barriers. With 80% household literacy, we unlock ₹5 lakh crore in household savings entering formal financial systems, creating multiplier effects across rural economies. The foundation is strong—behaviour scores are already at 73%. Now we build upward, turning everyday money management into informed financial decision-making that transforms lives and communities.

Reference:

1. NABARD (National Bank for Agriculture and Rural Development). (2022). NABARD All India Rural Financial Inclusion Survey (NAFIS) 2021-22: Financial Literacy. Mumbai: NABARD. Data sourced from Table: "Proportion of Households Having Financial Literacy in the Agricultural Year 2021-22."

Disclaimers

1. AI-Assisted Writing

This article was written with assistance from Claude AI. While I've made every effort to ensure accuracy, there may be errors. I sincerely apologize for any mistakes.

2. Fictional Characters

The Mehta family and Priya Sharma are fictional characters created solely to make complex financial data accessible and engaging. All names are invented and any similarity to real persons is coincidental. If any content inadvertently causes offense, I sincerely apologize—no harm was intended.

3. Intent and Purpose

This article is written purely to:

- Encourage critical thinking, independent research, and data-driven analysis among readers

- Provide imaginary use cases to researchers to motivate them to think in different directions about monetary policy impacts

- Present real economic data in an accessible narrative format

This is NOT intended as:

- Financial advice (please consult a qualified financial advisor)

- A critique of any government policies, institutions, or individuals

- An endorsement of any particular borrowing or investment strategy

The analysis is based on publicly available data and academic research, presented objectively to foster informed discussion. If any content is interpreted as criticism, I sincerely apologize—that was never my intention.

4. Financial Disclaimer

Past economic conditions do not guarantee future results. The scenarios presented are simplified for educational purposes. Real-world financial decisions should be made after consulting with qualified financial professionals and considering your complete financial situation.

Author's Note: If you found this helpful, please verify the data independently and consult professional financial advisors before making major financial decisions. The goal here is to spark curiosity and encourage deeper investigation into how monetary policy affects our daily lives.