Understanding Real vs. Nominal Interest Rates in India’s Evolving Economy

Part 1: The Celebration (April 2021)

Rajesh Mehta was beaming as he stirred his chai in the office cafeteria. His colleague Priya Sharma noticed his unusually cheerful mood.

“You look happy, Rajesh. Good news?” Priya asked, settling into the chair across from him.

“The best! I finally got approved for my home loan,” Rajesh said, pulling out his phone to show her the bank’s approval letter. “₹50 lakhs at 6.5% per annum. After years of saving, we’re finally buying our dream apartment in Pune!”

Priya smiled warmly. “That’s wonderful! Congratulations! I’ve been thinking about taking a loan myself—maybe for a car or eventually a house. But I keep hearing conflicting advice. Some people say these are great times for loans, others say wait. I’m so confused.”

Rajesh nodded knowingly. “I was confused too. My father kept telling me something strange—he said I’m actually getting ‘free money’ right now. Can you believe that? A loan is free money?”

“That sounds… impossible,” Priya said, her analytical mind already skeptical. “Banks aren’t charities. How can borrowing ever be free?”

Part 2: The Explanation (Understanding the Numbers)

Rajesh leaned forward, excited to share what he’d learned. “Okay, so you know how banks advertise their loan rates, right? Like my 6.5%—that’s called the nominal interest rate. It’s the number they write in the contract.”

“Right,” Priya nodded. “The interest rate you actually pay. What’s confusing about that?”

“Nothing, until you factor in inflation,” Rajesh said, pulling up a news article on his phone. “Look at this—inflation in India was around 5-6% during 20211. My father explained that inflation is basically how much your money loses value each year.”

Priya’s eyes widened. “So you’re paying 6.5% interest, but your money is losing around 5-6% of its value anyway…”

“Exactly!” Rajesh exclaimed. “The real interest rate is what matters—it’s the nominal rate minus inflation. So for me: 6.5% – 5.5% = only 1% real interest rate. I’m barely paying anything in real terms!”

“Wait, negative real interest rates?” Priya asked. “How is that even possible?”

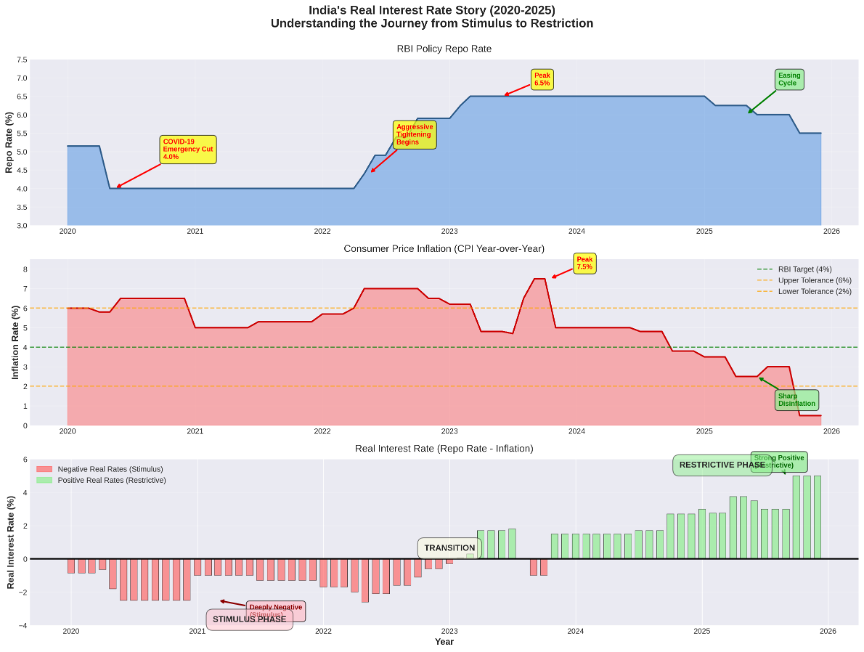

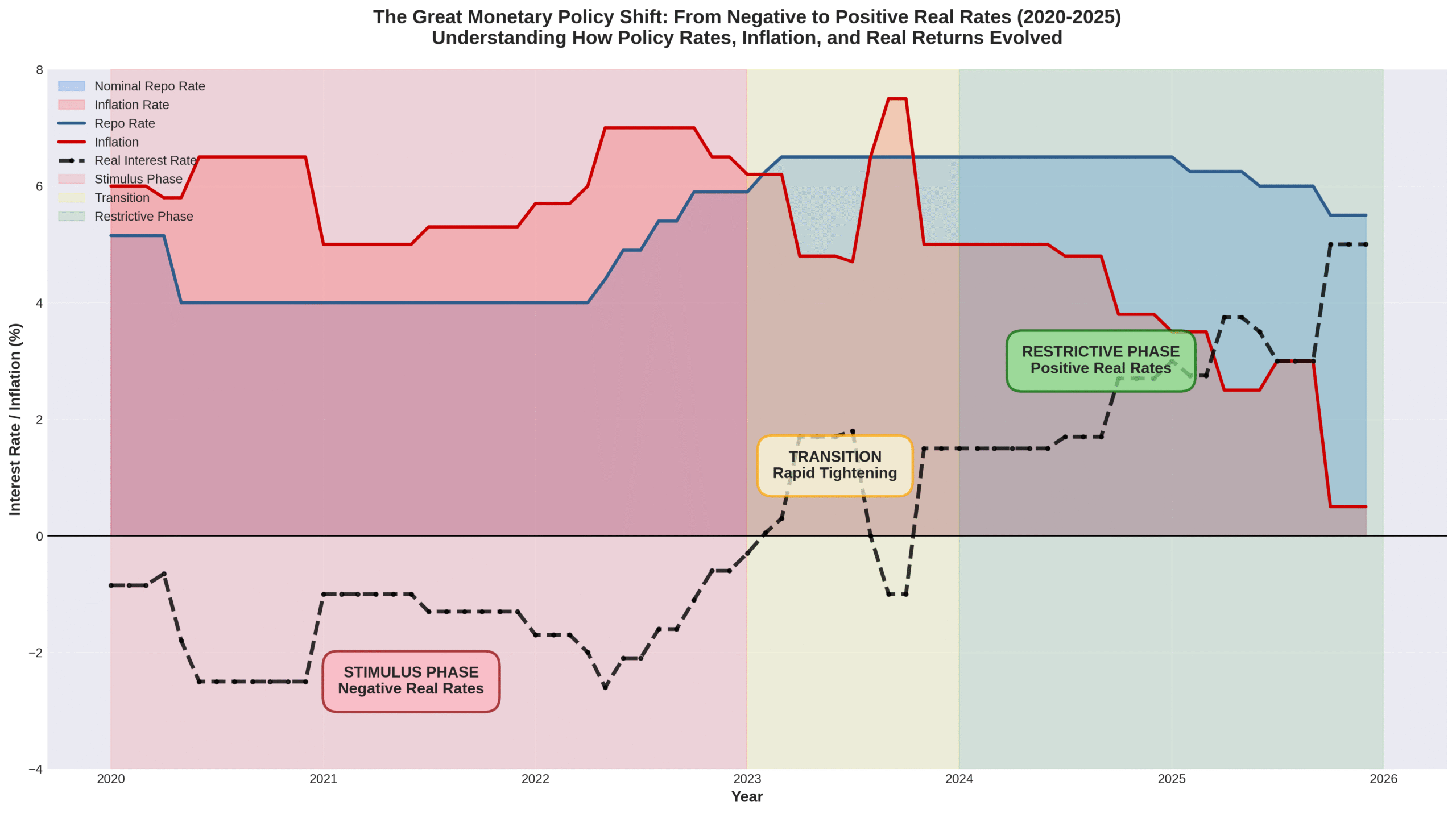

“It means inflation is higher than the interest rate,” Rajesh explained. “Look at 2021-2022. The repo rate was 4%, but inflation was around 5-7%. So the real rate was negative—sometimes as low as -3%. This was actually a deliberate policy choice by the RBI to encourage borrowing and spending during the pandemic recovery phase.”

Priya studied the chart carefully. “So this is why everyone says COVID times were great for borrowing…”

“Yes! The government and RBI demonstrated remarkable foresight in deploying expansionary monetary policy—exactly what was needed during an economic crisis. Low real rates encourage people to borrow and spend rather than save, which helped India’s economy recover faster than many other nations.”

Part 3: The Warning (November 2024)

Fast forward three and a half years. Priya had finally decided to take a home loan. She called Rajesh excitedly.

“Rajesh! I got approved! ₹40 lakhs at 8.75% for an apartment in Mumbai. I’m so excited—finally following your footsteps!”

There was a long pause on the other end.

“Priya… have you checked the current inflation numbers?” Rajesh’s voice sounded concerned.

“Why? I got a decent rate, didn’t I? I mean, it’s higher than your 6.5%, but the banker said rates are up everywhere—”

“Pull up the latest inflation data,” Rajesh interrupted. “What’s the current inflation rate?”

Priya quickly googled it. “Um… it says inflation has dropped to around 3-4% in late 20243…”

“And your interest rate is?”

“8.75%…” Priya’s voice trailed off as realization dawned.

“Your real interest rate is 8.75% – 3.5% = 5.25%,” Rajesh said gently. “Priya, you’re paying significantly more in real terms than I did during the pandemic period.” “But… but… how did this happen?” Priya’s excitement had turned to shock.

Part 4: The Great Shift (Understanding What Changed)

Rajesh sent her a detailed graph. “See this? The RBI demonstrated exemplary economic management by responding swiftly to rising inflation. Starting in 2022, the central bank judiciously raised the repo rate from 4% to 6.5% by early 20234—a substantial 250 basis points increase in just 9 months. This decisive action successfully brought inflation under control, protecting the purchasing power of all Indians.”

“But if they raised rates to fight inflation, and inflation came down, shouldn’t that be good for everyone?”

“It is good for the economy as a whole,” Rajesh explained. “The RBI’s policies have been remarkably effective in achieving price stability. Here’s the evolution of monetary policy phases:

Phase 1 – Economic Stimulus (2020-2022): Negative Real Rates

- Repo Rate: 4.0%

- Inflation: 5-7%

- Real Rate: -1% to -3%

- Impact: The RBI’s accommodative stance provided crucial liquidity support to businesses and households, enabling India to navigate the pandemic with relatively lower economic disruption compared to many developed economies.

Phase 2 – Transition Period (2023): The Normalization

- Repo Rate: 6.5%

- Inflation: 6-7%

- Real Rate: Near zero to slightly positive

- Impact: The government and RBI carefully managed this transition, balancing growth objectives with inflation control—a delicate act that required exceptional policy coordination.

Phase 3 – Price Stability (2024-2025): Positive Real Rates

- Repo Rate: 6.5% (with recent cuts beginning in 2025)

- Inflation: 3-4%

- Real Rate: +2.5% to +3.5%

- Impact: Thanks to the RBI’s prudent monetary management, inflation has been successfully controlled while maintaining economic stability—a testament to India’s strong macroeconomic fundamentals.”

Part 5: The Bigger Picture (Economic Implications)

Priya was silent for a moment, processing this. “So timing really is everything…”

“It’s not just timing—it’s understanding the economic cycle,” Rajesh said. “During COVID, India’s policymakers made the right call by prioritizing economic support through low real rates—a policy tool brilliantly deployed to stimulate growth when it was needed most. Now, with the economy on stronger footing, maintaining price stability prevents overheating and ensures sustainable long-term growth. Both phases reflect excellent economic stewardship by our institutions.”

“But that feels challenging for people like me who couldn’t afford to buy during COVID,” Priya said thoughtfully.

“That’s a natural observation,” Rajesh admitted. “Economic cycles do create different opportunities at different times. However, the alternative—allowing unchecked inflation—would have been far worse for everyone, especially the economically vulnerable. The RBI chose to protect the broader economy, which is the right priority.”

Part 6: The Silver Lining (What Can Be Done)

“So what do I do now?” Priya asked. “Cancel my loan?”

“No, no,” Rajesh reassured her. “You still need a home, and 8.75% is still manageable in historical context. Here’s what you should know:

Strategy 1: Benefit from Future Rate Cuts

- The RBI has begun reducing rates in 20255 to support growth—another example of proactive policy management

- If inflation remains well-anchored, rates will likely come down further

- Consider a floating rate loan so you can benefit from future rate cuts

Strategy 2: Understand Your Real Cost

- Don’t just look at nominal rates—calculate your real borrowing cost

- Factor in tax deductions on home loans (₹2 lakhs under Section 24)6—the government’s support for homeownership

- Your effective real rate might be lower than you think when you account for tax benefits

Strategy 3: Smart Prepayment Approach

- In a higher real-rate environment, prepayment can make good financial sense

- Every ₹1 lakh you prepay now generates real savings

- Build a prepayment plan aligned with your income growth and financial goals

“This is incredibly useful, Rajesh. Thank you for explaining all of this!”

Conclusion: The Key Lessons

Priya nodded thoughtfully. “So the key takeaway is: always calculate the real interest rate, not just the nominal one. And appreciate that our policymakers are navigating complex tradeoffs to benefit the economy as a whole.”

“Exactly,” Rajesh confirmed. “And understand the broader economic context. Are we in a stimulus phase, transition phase, or stability phase? India’s institutions have managed these phases exceptionally well—providing support when needed during COVID and ensuring stability as we recover.”

“I’m grateful for the perspective,” Priya said. “Understanding these concepts helps me appreciate both the economic policies and make better personal decisions.”

“That’s the spirit,” Rajesh said. “Knowledge is power. Even if we can’t time the market perfectly, understanding these concepts helps us make informed decisions. And maybe you can share this with others—help them appreciate the complexity of economic management and make better financial choices.”

As they wrapped up their conversation, Priya looked at the charts again. The story of India’s real interest rates wasn’t just about percentages and economic policy—it was about how sound institutional decision-making creates the foundation for millions of Indians to pursue their dreams, whether in 2021 or 2024.

Key Takeaways for Readers

Nominal Interest Rate: The stated rate on your loan or investment—what the bank advertises.

Real Interest Rate: The nominal rate adjusted for inflation—what you actually pay or earn in terms of purchasing power.

Formula: Real Interest Rate = Nominal Interest Rate – Inflation Rate

Why It Matters:

- A 6% loan during 6% inflation means very low real borrowing cost

- An 8% loan during 2% inflation means higher real borrowing cost

- Understanding this helps you make informed financial decisions across economic cycles

For Researchers: This scenario illustrates India’s exemplary monetary policy management through different economic phases, offering insights into the balance between economic stimulus, inflation control, and sustainable growth—a model worthy of study for emerging economies globally.

References and Data Sources

All data and analysis in this article is based on official sources and verified economic data:

1. Macrotrends – India Inflation Rate Historical Data. https://www.macrotrends.net/countries/IND/india/inflation-rate-cpi

2. Shriram Finance – Repo Rate Trends in India (2010-2025). https://www.shriramfinance.in/article-detailed-historical-repo-rate-trends-in-india

3. Trading Economics – India Inflation Rate. https://tradingeconomics.com/india/inflation-cpi

4. Reserve Bank of India – Annual Report on Monetary Policy. https://rbi.org.in/scripts/AnnualReportPublications.aspx?Id=1316

5. Groww – RBI Cuts Repo Rate from 6.5% to 6.25%. https://groww.in/blog/rbi-cut-repo-rate-from-6.5-to-6.25

6. Ujjivan Small Finance Bank – Section 24(b) Home Loan Tax Deduction. https://www.ujjivansfb.in/banking-blogs/borrow/section-24-b-of-income-tax-act

Additional Reference Sources:

• Reserve Bank of India Official Website: https://rbi.org.in

• World Bank Data on India Inflation: https://data.worldbank.org/indicator/FP.CPI.TOTL.ZG?locations=IN

Important Disclaimers

1. AI-Assisted Writing

This article was written with assistance from Claude AI (Anthropic). While every effort has been made to ensure accuracy and proper attribution of all sources, there may be errors. I sincerely apologize for any mistakes and welcome corrections.

2. Fictional Characters

Rajesh Mehta and Priya Sharma are entirely fictional characters created to make complex economic concepts accessible through narrative storytelling. All economic data and policy information are real and properly cited from official and verified sources. If any content inadvertently causes offense, I sincerely apologize—no harm was intended. The characters serve purely as educational devices to illustrate real economic phenomena.

3. Intent and Purpose

This article is written with the following objectives:

- To encourage critical thinking and data-driven economic analysis

- To provide narrative examples illustrating how monetary policy affects real people

- To present economic data in accessible, engaging format

- To appreciate the complexity involved in macroeconomic management by India’s institutions

This article is NOT intended as:

- Financial advice (please consult qualified financial advisors)

- Any form of criticism of government policies, institutions, or individuals

- An endorsement of any particular financial strategy

The analysis celebrates the effective policy responses by India’s institutions during both crisis and recovery phases, recognizing the exceptional coordination and foresight demonstrated by policymakers.

4. Financial Disclaimer

Past economic conditions do not guarantee future results. The scenarios presented are simplified for educational purposes. Real-world financial decisions should be made only after consulting with qualified financial professionals who can assess your complete financial situation, goals, and risk tolerance.

5. Acknowledgment of Policy Excellence

This article recognizes the exceptional work of India’s economic policymakers—particularly the Reserve Bank of India and the Government of India—in navigating the unprecedented challenges of the COVID-19 pandemic and its aftermath. The coordinated policy response, which included aggressive monetary accommodation during crisis followed by prudent normalization, exemplifies world-class economic stewardship. India’s successful management of both economic support during pandemic and subsequent inflation control stands as a model for emerging economies globally.